Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Talking on the Financial institution of America Housing Symposium in June 2025, Toll Brothers CEO Doug Yearley—who has since stepped down—acknowledged that parts of Arizona, Florida, and Texas were dealing with spec inventory “overhangs” that he stated would finally “clear up [over time] as a result of the builders are beginning fewer spec properties within the softer market, and I feel that may naturally work its manner out.”

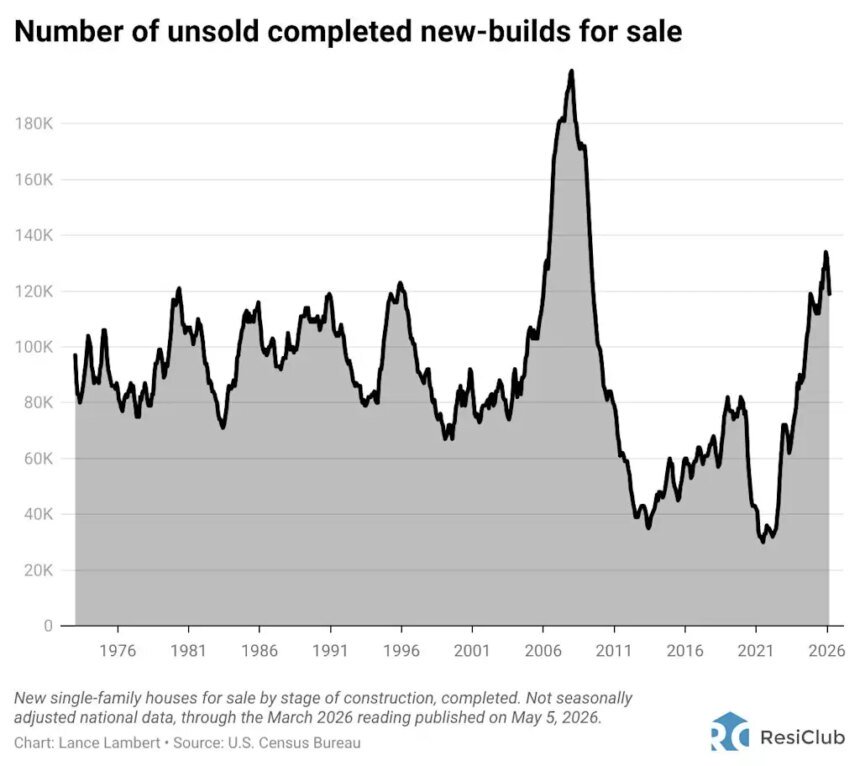

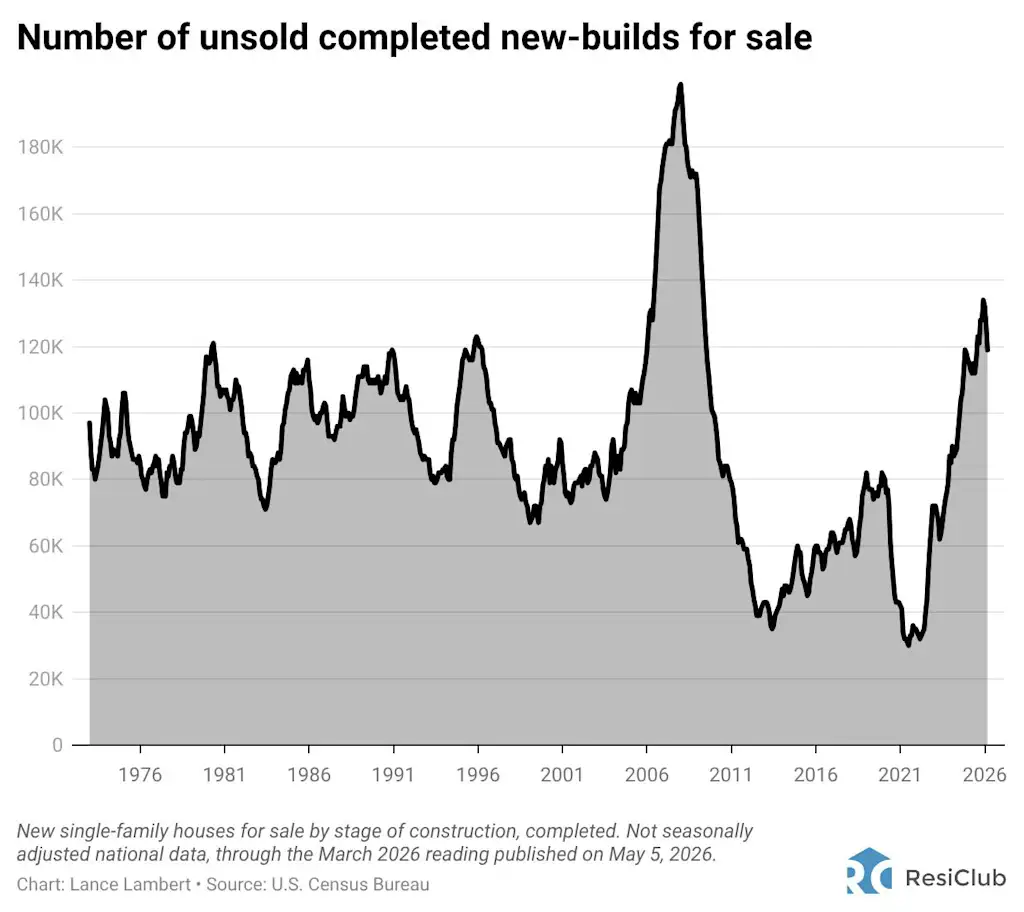

On the peak of the pandemic housing growth, when practically every thing homebuilders had been constructing was flying off the cabinets, there have been solely 32,000 unsold completed new-build homes in March 2022. As soon as the growth fizzled out, that determine rapidly started to rebound—particularly in Sunbelt boomtowns—reaching a excessive of 134,000 unsold accomplished new-build properties by December 2025.

Nonetheless, information revealed this week exhibits that the variety of unsold accomplished new-build properties has, at the very least for now, fallen to 119,000 as of March 2026. Whereas the depend of unsold accomplished new-build properties continues to be up 12 months over 12 months (there have been 113,000 unsold accomplished in March 2025), the decline over the previous few months has been bigger than seasonality alone would recommend.

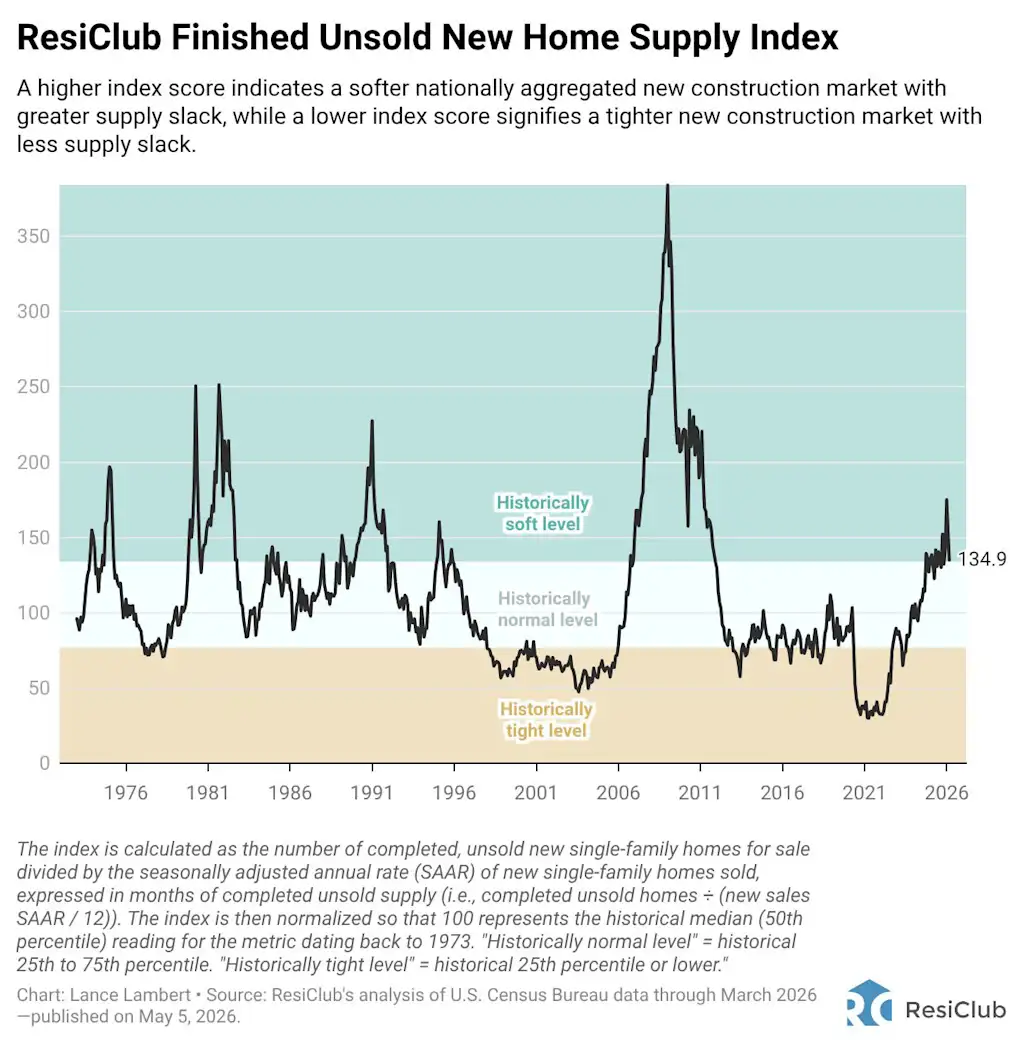

To place the variety of unsold accomplished new single-family properties into higher historic context, now we have the ResiClub Completed Unsold New Properties Provide Index. It accounts for unsold accomplished stock relative to new house gross sales. The next index rating signifies a softer nationwide new development market with higher provide slack, whereas a decrease index rating signifies a tighter new development market with much less provide slack. Over the previous few months, that studying has nearly drifted again down into the “traditionally regular” vary.

After experiencing a softer 2025 than anticipated—and greater-than-expected margin compression—many big homebuilders instructed analysts heading into 2026 that they’d pivot toward fewer spec builds and more build-to-order homes. The explanation was easy: Construct-to-order margins are materially greater. Constructed-to-order properties are likely to generate greater margins as a result of they’re offered earlier than development begins, decreasing stock carrying prices and the danger of getting to deploy bigger incentives to promote them.

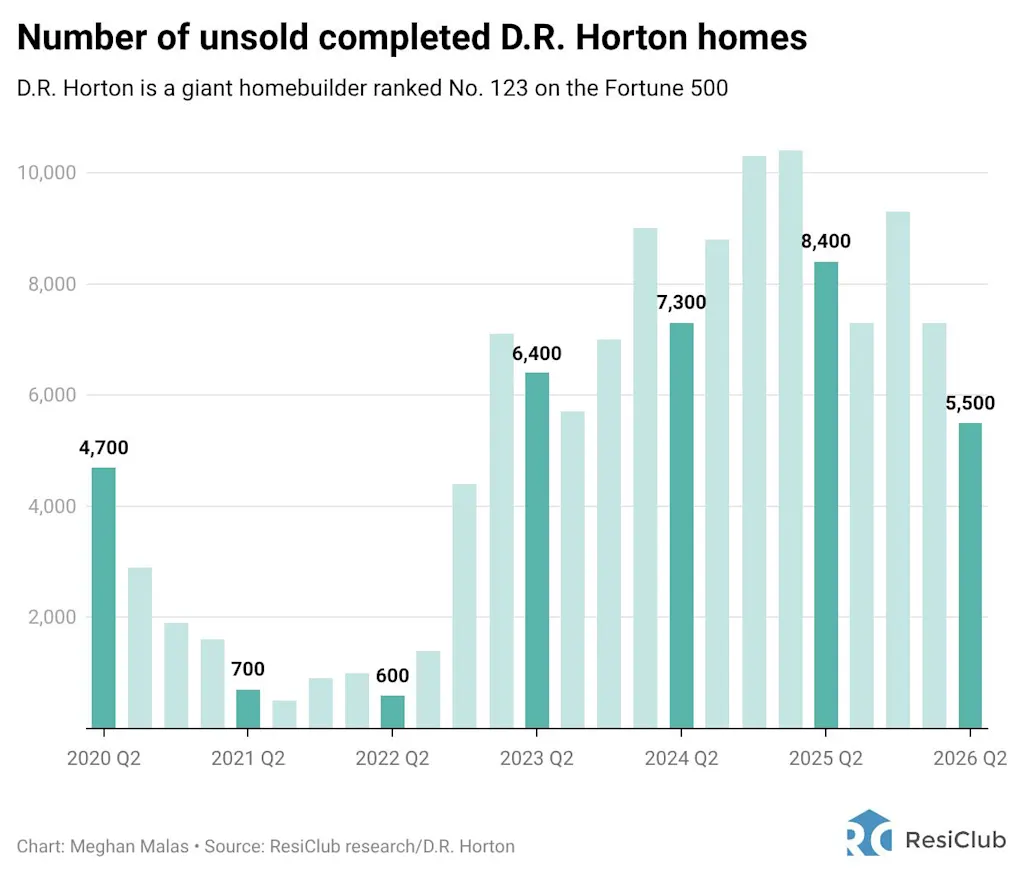

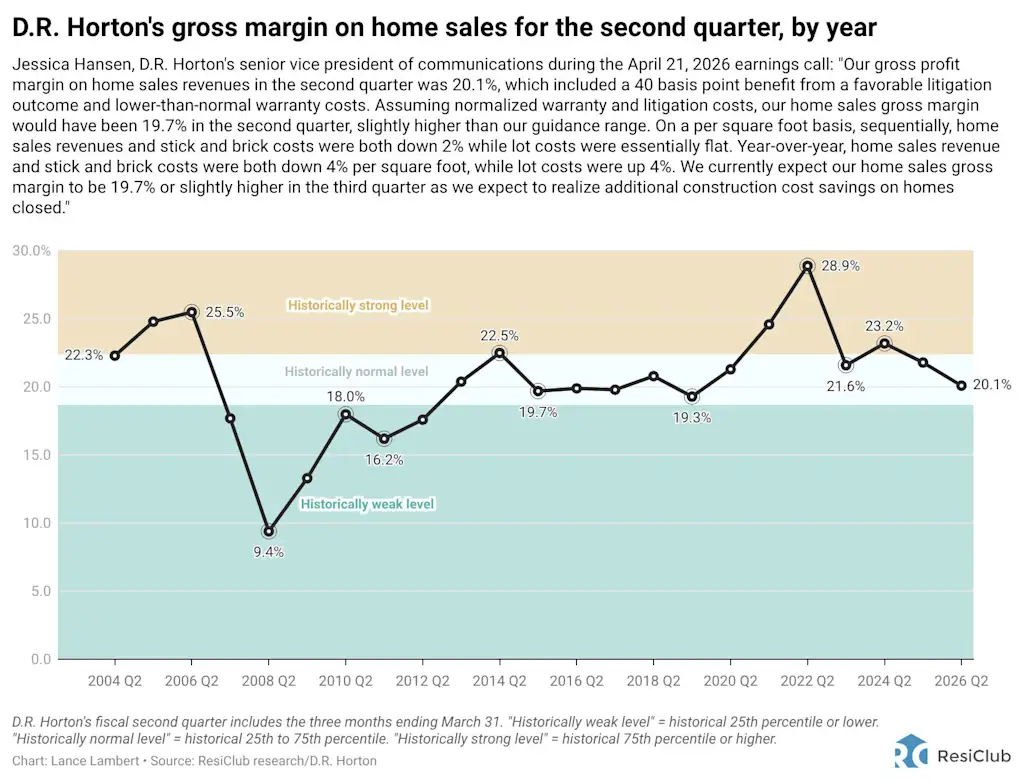

Doing fewer specs and begins in softer pockets of the Sunbelt has already helped a few of the builders scale back their depend of unsold accomplished properties. Simply have a look at America’s largest homebuilder, D.R. Horton.

Right here’s what Paul Romanowski, CEO of D.R. Horton, said throughout the firm’s April 21, 2026 earnings name:

“Unsold properties [for us] are down 25% from December and 35% from a 12 months in the past, with each unsold properties as a share of whole stock and accomplished unsold stock at their lowest ranges since fiscal 2023 for properties closed within the second quarter.

“We anticipate begins within the third quarter to be decrease than the second quarter, and we’ll proceed to handle our stock ranges and begin area primarily based on market circumstances.”

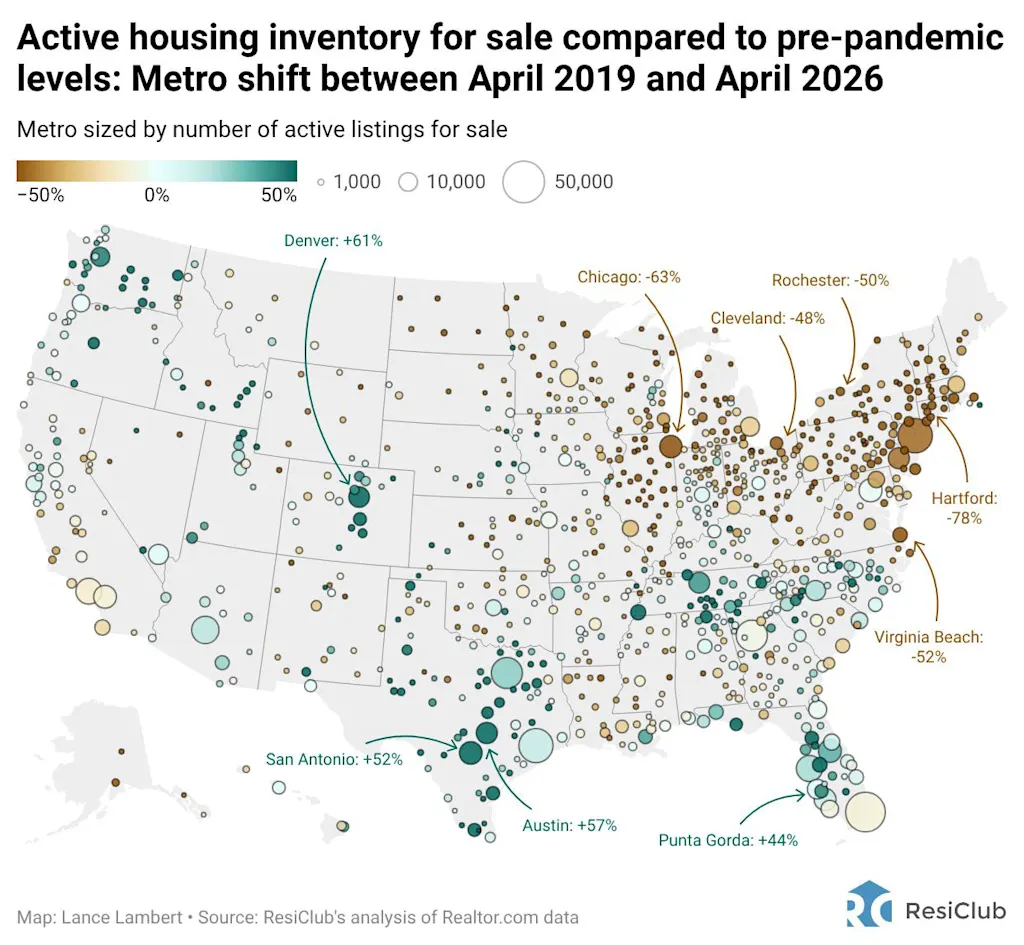

Whereas the U.S. Census Bureau doesn’t give us a higher market-by-market breakdown on these unsold accomplished new builds, now we have a good suggestion the place they’re, primarily based on whole energetic stock properties on the market (together with present)—seemingly a lot of it’s within the Mountain West and the Sunbelt, significantly across the Gulf.

We must always level out that whereas many markets in Texas and Florida skilled a big put up–pandemic housing growth stock bounce-back, that stock development has decelerated in latest months. In reality, many components of Florida are actually seeing year-over-year energetic stock on the market declines. The heavy discounting by homebuilders in weaker pockets of Texas and Florida to maneuver unsold stock—mixed with diminished housing begins and fewer spec builds in these pockets heading into 2026—has, partly, contributed to that slowdown in stock development.

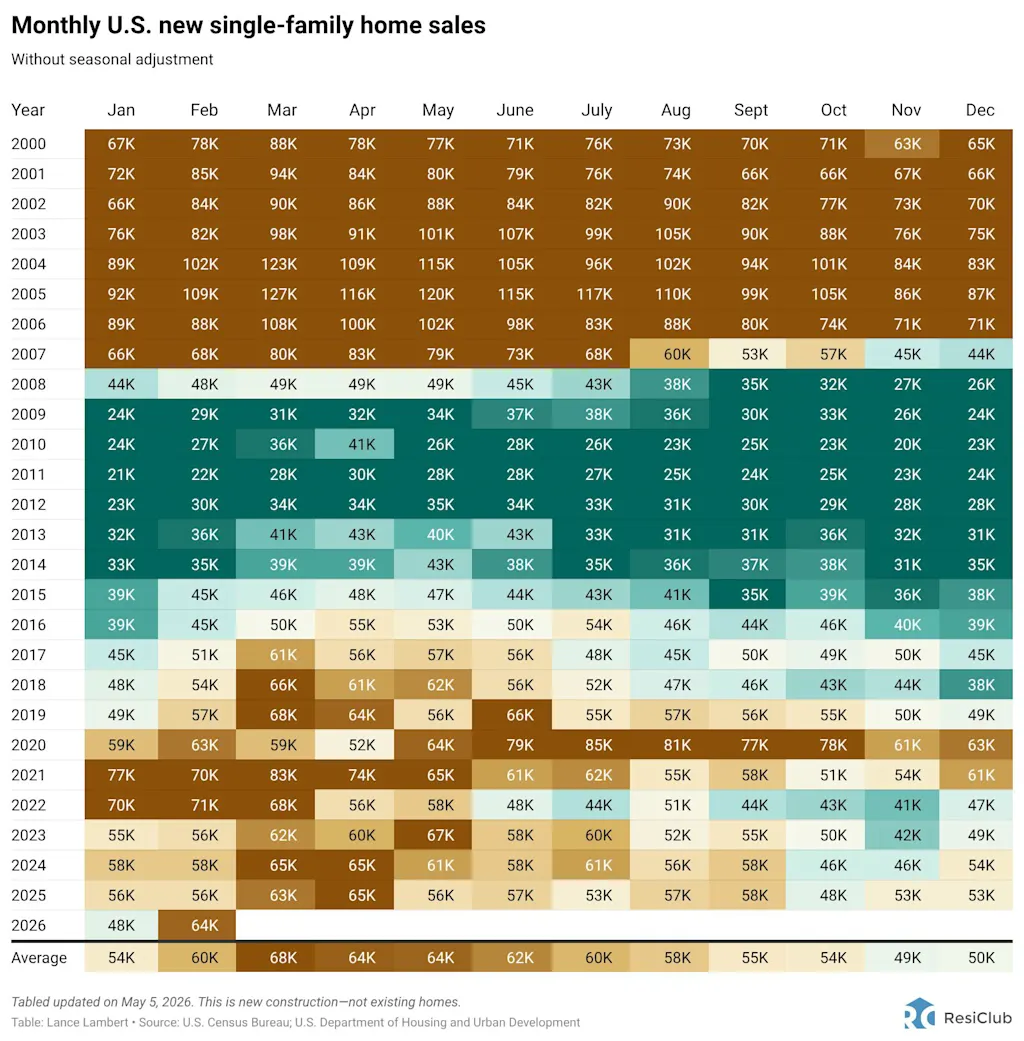

Not like the existing-home market—the place U.S. existing-home gross sales are nonetheless -23.6% under pre-pandemic 2019 ranges—U.S. new-home gross sales are basically on par with pre-pandemic 2019 ranges proper now 👇

Why haven’t U.S. new house gross sales come down extra, given the affordability image and what’s occurred within the existing-home market?

A number of it boils right down to the truth that many homebuilders for the reason that pandemic housing growth fizzled out have accomplished bigger affordability changes—together with every thing from larger buydowns, extra money again at shut, and even outright worth cuts—so as to preserve transferring product once they run into softness in a given neighborhood. Probably the most aggressive homebuilder on the motivation entrance is Lennar. Final quarter, Lennar spent the equal of 14% of the ultimate gross sales worth on gross sales incentives. For a $400,000 house, that interprets to $56,000 in incentives. Lennar’s cycle low was in Q2 2022, when it spent 1.5% of the ultimate gross sales worth on gross sales incentives.

As a way to do larger incentives—and pay for sticky land costs—homebuilders have been compressing margins. Certainly, all 11 of the most important publicly traded U.S. homebuilders that ResiClub tracks probably the most intently have seen year-over-year gross margin compression.

So in different phrases, massive homebuilders have been prepared to regulate costs and incentives so as to preserve gross sales quantity, whereas existing-home sellers, in combination, have fought tougher towards worth changes—on the expense of pace of sale and turnover. One other issue is that homebuilders’ willingness to promote isn’t impacted by so-called affordability “lock-in.” Ever since mortgage charges spiked, excessive switching prices have left many owners both unwilling or unable to promote and purchase at as we speak’s costs and charges, additional suppressing existing-home turnover.

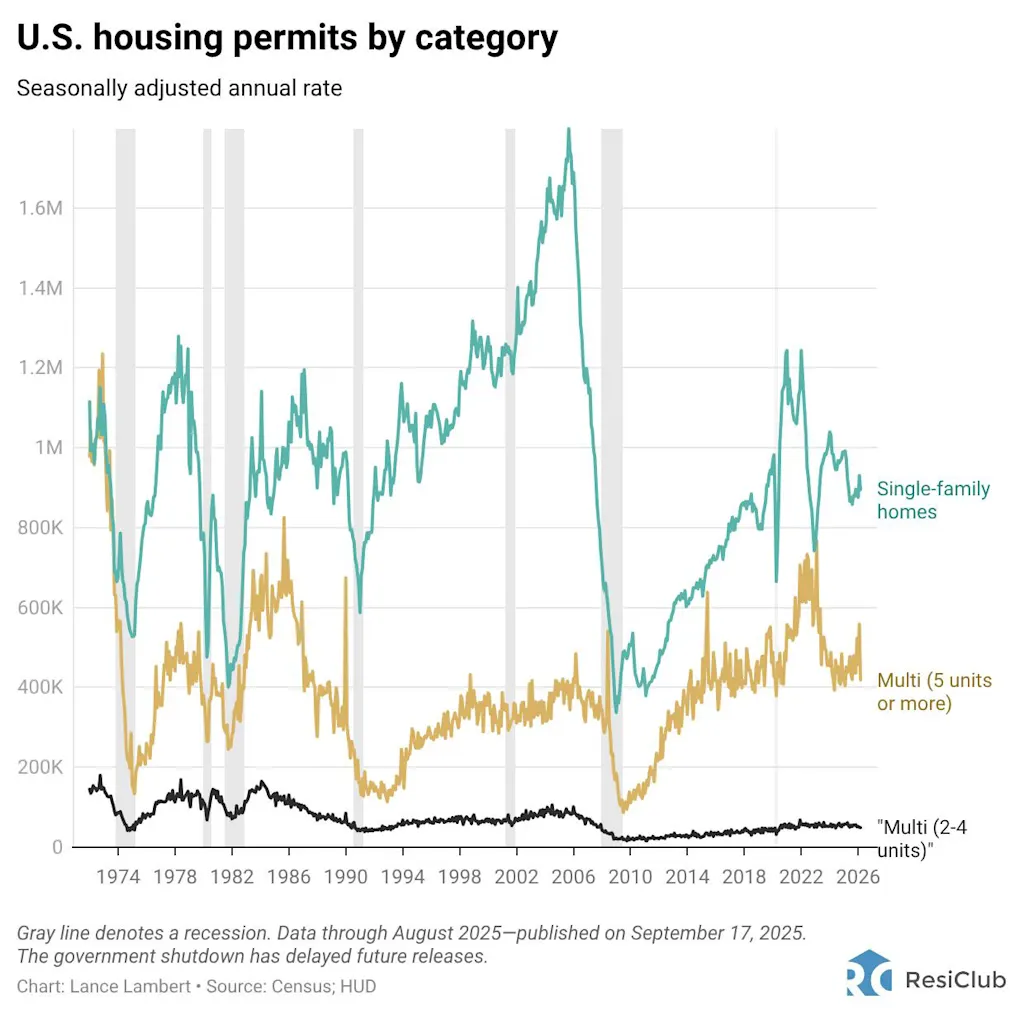

Earlier than we conclude as we speak’s new development report, right here’s a historic have a look at nationally aggregated permits.

{kind=link}