Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Primarily based on our evaluation of the Zillow House Worth Index, U.S. residence costs—together with single-family and condos—rose 0.8% between Might 2025 and Might 2026. That tempo is about the identical because it was a yr in the past, again in Might 2025, when the nationwide year-over-year residence value progress charge was 0.4%. And it’s up barely from the current year-over-year low of -0.01% in August 2025.

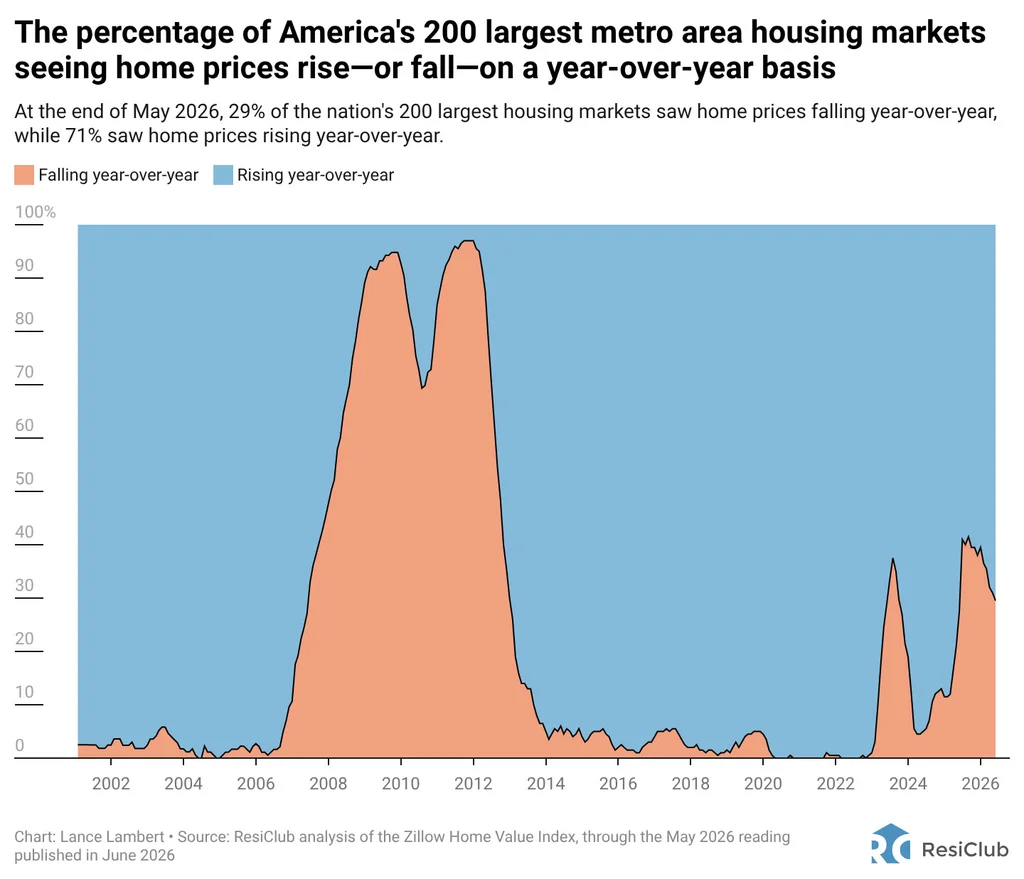

Within the first half of 2025, the variety of main metro space housing markets seeing year-over-year declines climbed. That rely has since stopped ticking up.

- 31 of the nation’s 300 largest housing markets (10% of markets) had a falling year-over-year studying within the January 2024 to January 2025 window.

- 42 of the nation’s 300 largest housing markets (14%) had a falling year-over-year studying within the February 2024 to February 2025 window.

- 60 of the nation’s 300 largest housing markets (20%) had a falling year-over-year studying within the March 2024 to March 2025 window.

- 80 of the nation’s 300 largest housing markets (27%) had a falling year-over-year studying within the April 2024 to April 2025 window.

- 96 of the nation’s 300 largest housing markets (32%) had a falling year-over-year studying within the Might 2024 to Might 2025 window.

- 110 of the nation’s 300 largest housing markets (36%) had a falling year-over-year studying within the June 2024 to June 2025 window.

- 105 of the nation’s 300 largest housing markets (36%) had a falling year-over-year studying within the July 2024 to July 2025 window.

- 109 of the nation’s 300 largest housing markets (35%) had a falling year-over-year studying within the August 2024 to August 2025 window.

- 105 of the nation’s 300 largest housing markets (35%) had a falling year-over-year studying within the September 2024 to September 2025 window.

- 105 of the nation’s 300 largest housing markets (35%) had a falling year-over-year studying within the October 2024 to October 2025 window.

- 98 of the nation’s 300 largest housing markets (33%) had a falling year-over-year studying within the November 2024 to November 2025 window.

- 106 of the nation’s 300 largest housing markets (35%) had a falling year-over-year studying within the December 2024 to December 2025 window.

- 100 of the nation’s 300 largest housing markets (33%) had a falling year-over-year studying within the January 2025 to January 2026 window.

- 99 of the nation’s 300 largest housing markets (i.e., 33%) had a falling year-over-year studying within the February 2025 to February 2026 window.

- 89 of the nation’s 300 largest housing markets (30%) had a falling year-over-year studying within the March 2025 to March 2026 window.

- 81 of the nation’s 300 largest housing markets (27%) had a falling year-over-year studying within the April 2025 to April 2026 window.

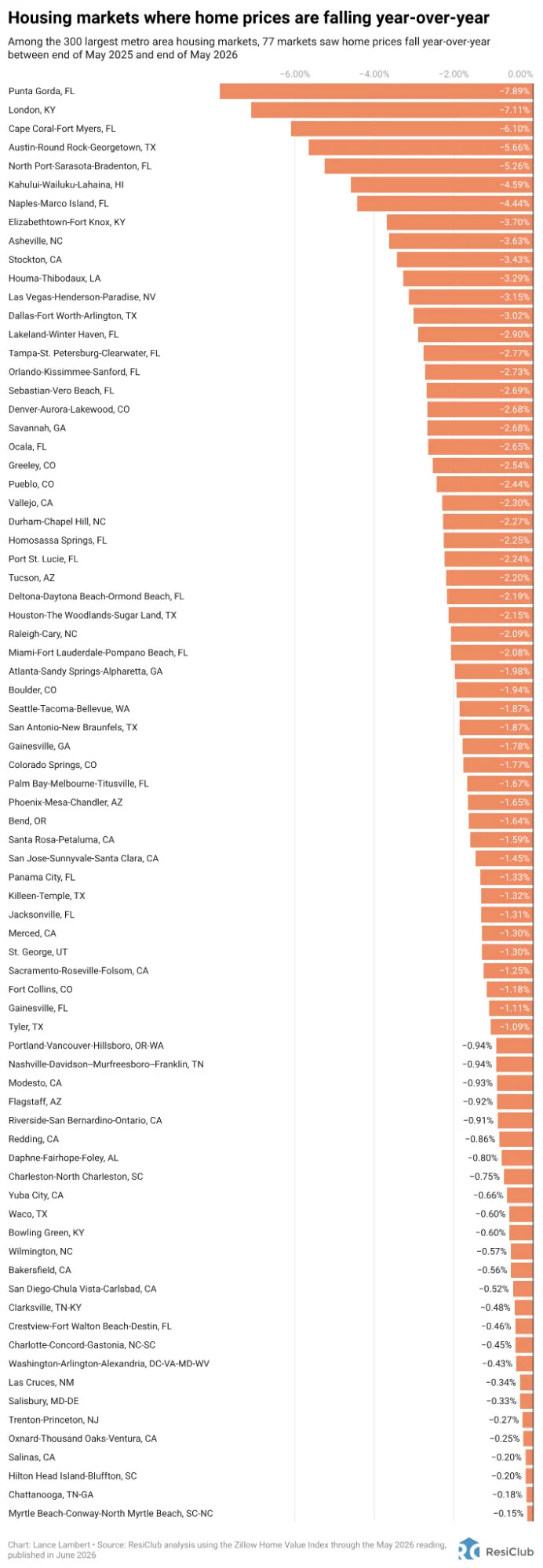

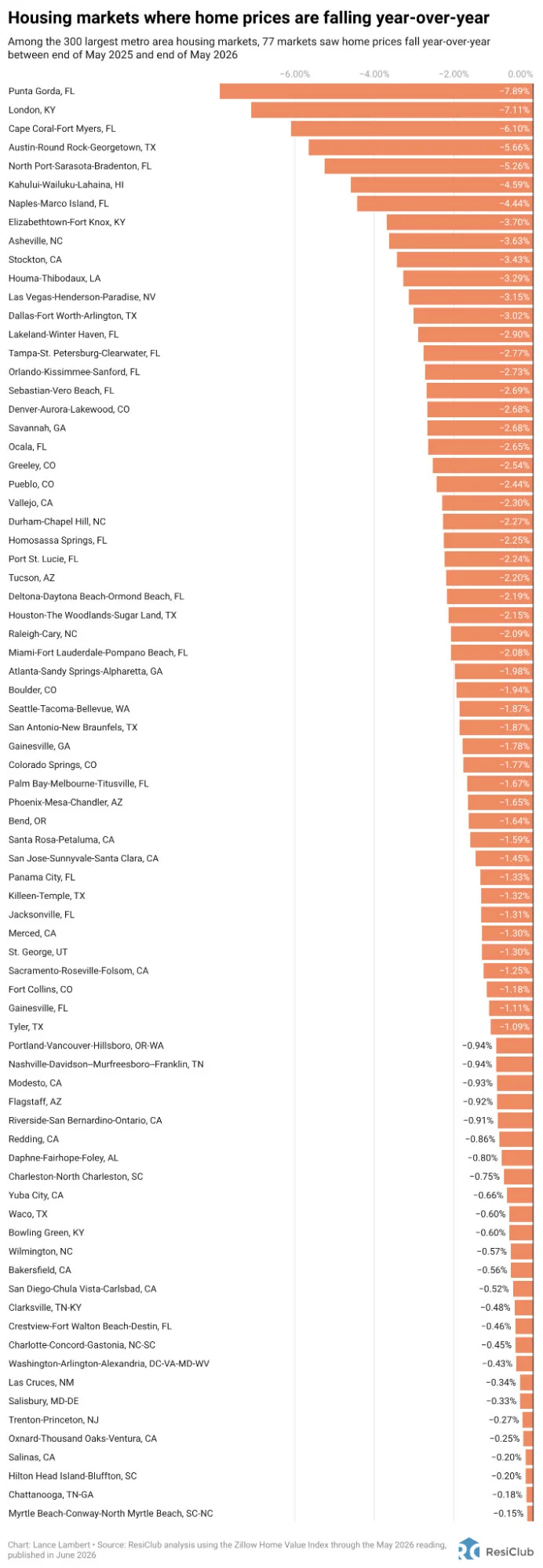

- 77 of the nation’s 300 largest housing markets (26%) had a falling year-over-year studying within the Might 2025 to Might 2026 window.

As you possibly can see above, within the first half of 2025, there was a notable enhance within the variety of housing markets slipping into year-over-year value declines as the supply–demand equilibrium (as measured by stock) shifted towards homebuyers. Over the previous 11 months, nonetheless, the record of declining markets has begun to stabilize and stock progress has decelerated.

Among the many 77 main metro space housing markets seeing falling year-over-year residence costs, these had the most important declines: Punta Gorda, Florida (-7.9%); London, Kentucky (-7.1%); Cape Coral, Florida (-6.1%); Austin (-5.7%); North Port, Florida (-5.3%); Kahului, Hawaii (-4.6% ); and Naples, Florida (-4.4%).

Again in fall 2025, ResiClub advised readers that we anticipated the rely of the variety of markets with year-over-year value declines to lower somewhat within the first half of 2026. That’s precisely what we’ve seen. It’s nonetheless very a lot a tender nationally aggregated housing market—however the burst of softening has let up.

House costs are nonetheless climbing somewhat year-over-year in lots of areas where active inventory remains well below prepandemic 2019 levels, equivalent to pockets of the Northeast and Midwest. In distinction, some pockets in states like Texas, Florida, and Colorado—the place energetic stock exceeds prepandemic ranges by a stable clip—are seeing modest residence value pullbacks or flat pricing.

(perform(){perform e(){window.addEventListener(`message`,perform(e){if(e.information[`datawrapper-height`]!==void 0){var t=doc.querySelectorAll(`iframe`);for(var n in e.information[`datawrapper-height`])for(var r=0,i;i=t[r];r++)if(i.contentWindow===e.supply){var a=e.information[`datawrapper-height`][n]+`px`;i.type.top=a}}})}e()})();

Housing markets seeing probably the most softness, the place homebuyers have gained probably the most leverage, are primarily in Solar Belt areas, notably the Gulf Coast and Mountain West.

Many of these areas saw even greater price surges during the pandemic housing boom, with residence value progress outpacing native revenue ranges. As pandemic-driven home migration slowed and mortgage charges rose in 2022, markets like Tampa, Florida, and Austin confronted challenges, counting on native revenue ranges to help frothy residence costs.

That Solar Belt softening was compounded by an abundance of recent residence provide. Builders are sometimes keen to decrease costs or provide affordability incentives to keep up gross sales, which has a cooling impact on the resale market. Consequently, some patrons who might need beforehand opted for present houses are as an alternative selecting new development with extra engaging offers—which added additional upward stress to resale stock progress over the previous few years.

After all, whereas 77 of the nation’s 300 largest metro space housing markets are seeing year-over-year residence value declines, one other 223 are seeing year-over-year residence value will increase.

The place are residence costs nonetheless up on a year-over-year foundation? See the map under.

(perform(){perform e(){window.addEventListener(`message`,perform(e){if(e.information[`datawrapper-height`]!==void 0){var t=doc.querySelectorAll(`iframe`);for(var n in e.information[`datawrapper-height`])for(var r=0,i;i=t[r];r++)if(i.contentWindow===e.supply){var a=e.information[`datawrapper-height`][n]+`px`;i.type.top=a}}})}e()})();

Under is a historic chart displaying the year-over-year change in residence costs throughout the 50 largest metro housing markets, with the yellow line representing the nationwide combination, relationship again to 2000.

Whereas the vary [see chart above] between the strongest and weakest metro space housing markets proper now could be pretty regular traditionally talking, the “bifurcation” —the share of markets with rising residence costs versus these with falling costs—is wider than regular, on condition that nationwide appreciation has stabilized right into a softer market with progress barely above zero. And the longer some markets stay within the rising camp whereas others keep within the falling camp, the broader the gulf between the comparatively extra resilient markets and the weaker ones.

For instance, residence costs within the Hartford, Connecticut, metro space are actually +25.6% above their 2022 peak, whereas residence costs within the Austin metro space sit -27.3% under their 2022 peak. A few of that bifurcation boils right down to reversion to the imply, with lots of the residence value declines occurring in markets that overheated further during the pandemic boom.

Observe: For the historic chart under, we analyzed the 200 largest markets reasonably than the 300 used above, as some markets ranked 201 to 300 lack full information going again to 2000. When weighted by inhabitants (not visualized), the housing market seems barely weaker than the chart under suggests—which aligns with the truth that, amongst simply the 50 largest housing markets, 22 (44%) are posting year-over-year value declines, and nationally aggregated residence costs are up simply 0.8% year-over-year utilizing the Zillow House Worth Index.

{kind=link}