Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

When assessing residence value momentum, ResiClub believes it’s necessary to watch energetic listings and months of provide. If energetic listings begin to improve quickly as houses stay in the marketplace for longer intervals, it might point out pricing softness or weak point. Conversely, a fast decline in energetic listings past seasonality may recommend a market the place sellers are gaining energy.

Because the nationwide pandemic housing growth fizzled out in 2022, the ability dynamic has slowly been shifting directionally from sellers to patrons. In fact, that shift has different throughout the nation.

Usually talking, native housing markets the place energetic stock has jumped above pre-pandemic 2019 ranges have experienced softer home price growth (or outright value declines) over the previous 47 months. Conversely, native housing markets the place energetic stock stays far under pre-pandemic 2019 ranges have, usually talking, skilled, comparatively talking, extra resilient residence value progress over the previous 47 months.

The place is nationwide energetic stock headed now?

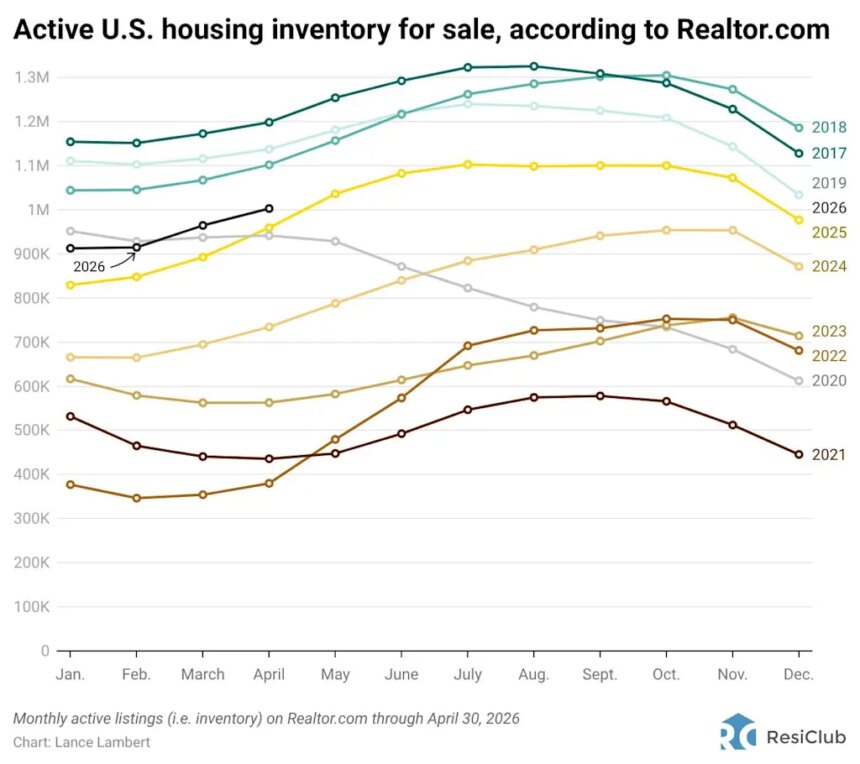

Whereas nationwide energetic stock remains to be up 12 months over 12 months, the tempo of progress has slowed in latest months as softening has slowed.

Nationwide energetic listings are up 4.6% on a year-over-year foundation from April 30, 2025, to April 30, 2026, in line with Realtor.com’s stock information. However in the event you return 12 months, that year-over-year nationwide stock progress fee was a lot increased (+30.6%).

After a interval through which leverage shifted extra towards homebuyers, the supply-demand equilibrium within the nationally aggregated housing market has been extra steady in latest months.

Nationally, we’re nonetheless under pre-pandemic 2019 stock ranges (-11.8% under April 2019) and a few resale markets, specifically chunks of the Midwest and Northeast, nonetheless stay tightish, comparatively talking.

April stock/energetic listings whole, in line with Realtor.com:

- April 2017 -> 1,198,424

- April 2018 -> 1,102,064

- April 2019 -> 1,137,198

- April 2020 -> 941,733

- April 2021 -> 435,663 (pandemic housing growth overheating)

- April 2022 -> 379,978 (pandemic housing growth overheating)

- April 2023 -> 562,966

- April 2024 -> 734,318

- April 2025 -> 959,251

- April 2026 -> 1,002,935

If we keep the present year-over-year tempo of stock progress (+43,684 houses on the market), we’d have 1,046,619 energetic stock come April 2027. (Be aware: That’s not a prediction—I’m simply displaying what the maths seems to be like if that tempo continues.)

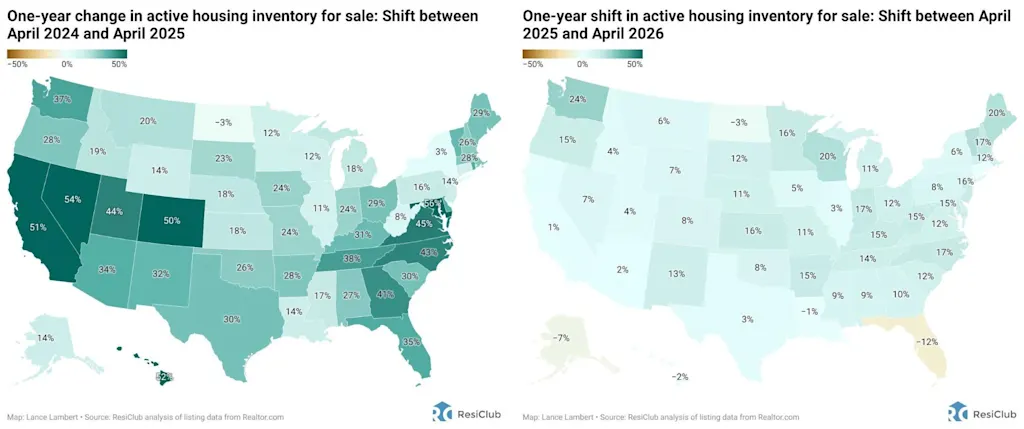

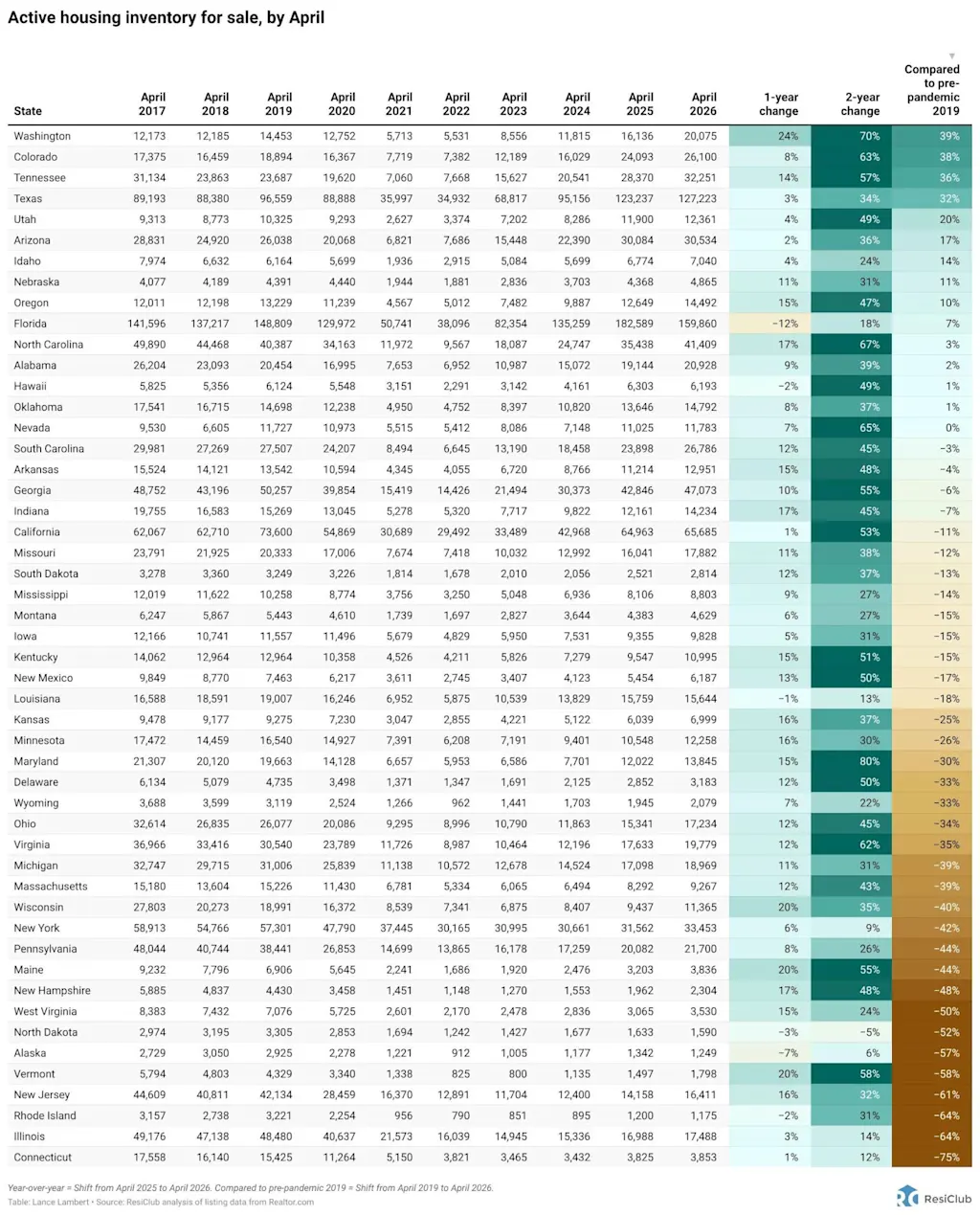

Under is the year-over-year energetic stock proportion change by state.

window.addEventListener(“message”,perform(a){if(void 0!==a.information[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.information[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.information[“datawrapper-height”][t]+”px”;r.type.top=d}}});

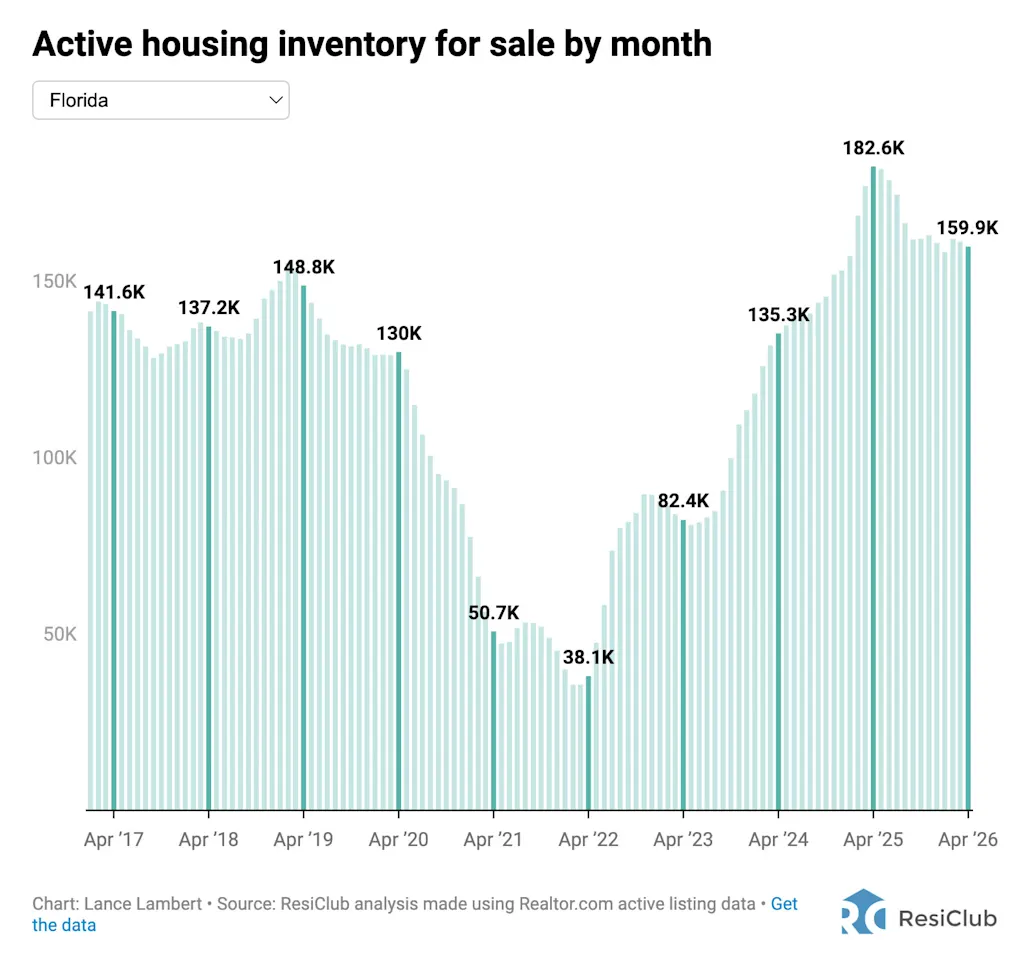

Whereas energetic housing stock is rising in most markets on a year-over-year foundation, the tempo of progress continues to decelerate throughout a lot of the nation (see the side-by-side maps under). Actually, Florida—residence to lots of the weakest regional housing markets over the previous two years—is now seeing energetic stock edge down just a little 12 months over 12 months (-12%).

Above, left: 12 months-over-year energetic stock shift from April 2024 to April 2025

Above, proper: Year-over-year active inventory shift from April 2025 to April 2026

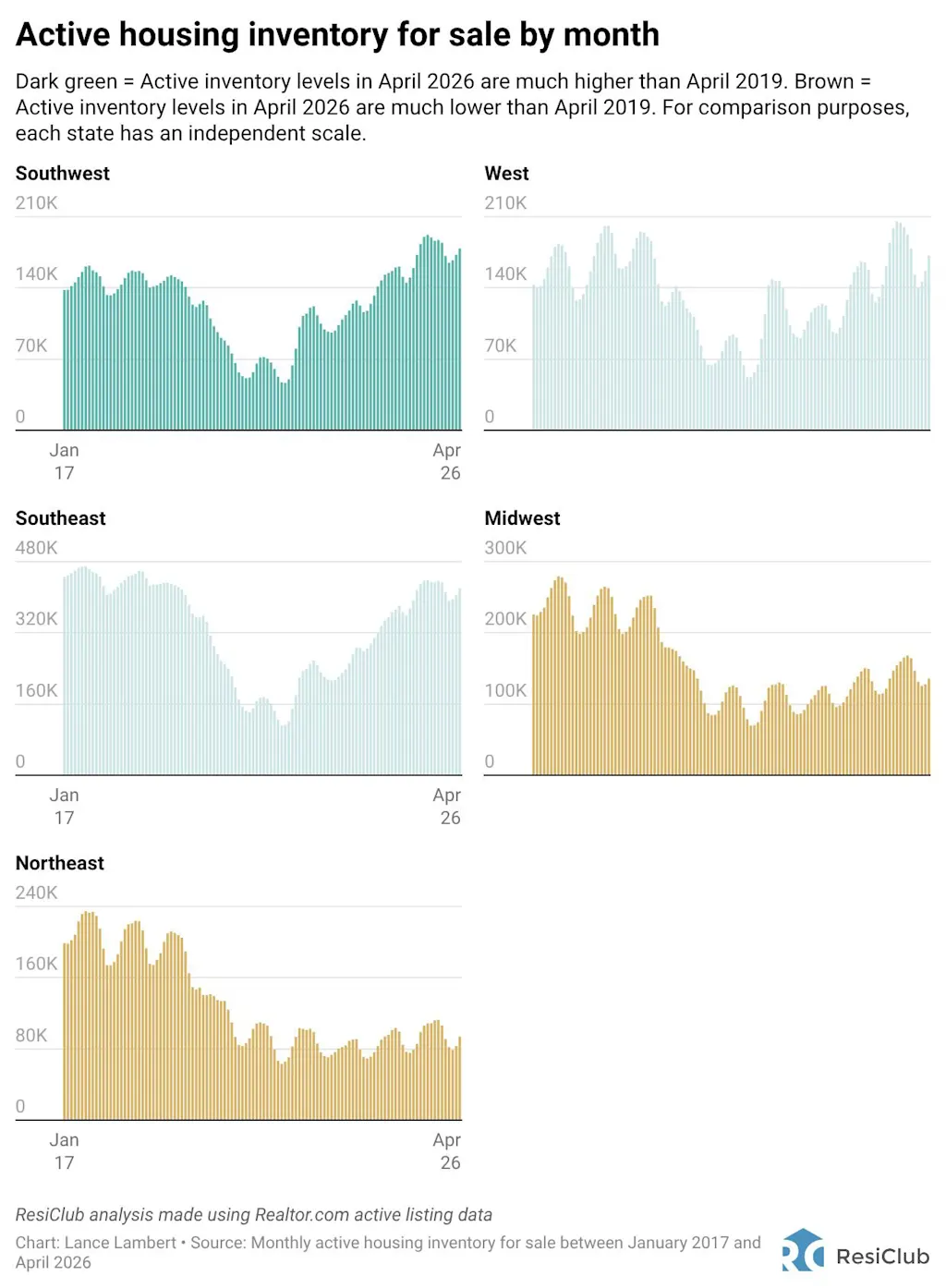

And whereas energetic housing stock is rising in most markets on a year-over-year foundation, some markets nonetheless stay tightish.

As ResiClub has been documenting, each energetic resale and new houses on the market stay probably the most restricted throughout enormous swaths of the Midwest and Northeast. That’s the place residence sellers within the spring/summer season are doubtless, comparatively talking, to have extra energy than their friends in lots of Southern markets.

Lively stock in April 2026 in comparison with pre-pandemic April 2019:

- Southwest —> +23%

- West —> +3%

- Southeast —> -2%

- Midwest —> -35%

- Northeast —> -50%

In distinction, energetic housing stock on the market has neared or surpassed pre-pandemic 2019 ranges in lots of components of the Sunbelt and Mountain West, together with metro space housing markets reminiscent of Punta Gorda, Florida, and Austin.

Many of those areas noticed main value surges throughout the pandemic housing growth, with residence costs getting stretched in comparison with native incomes. As pandemic-driven home migration slowed and mortgage charges rose, markets like Punta Gorda and Austin confronted challenges, counting on native earnings ranges to assist frothy residence costs.

This softening development was accelerated additional by an abundance of recent residence provide within the Sunbelt. Builders are sometimes keen to decrease costs or provide affordability incentives (if they’ve the margins to take action) to keep up gross sales in a shifted market, which additionally has a cooling impact on the resale market, with some patrons, who would have beforehand thought of present houses, choosing new houses with extra favorable offers over the previous couple years. That then places some further upward strain on resale stock.

Click here to view an interactive model of the map under.

window.addEventListener(“message”,perform(a){if(void 0!==a.information[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.information[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.information[“datawrapper-height”][t]+”px”;r.type.top=d}}});

On the finish of April 2026, 12 states had been above pre-pandemic 2019 energetic stock ranges: Alabama, Arizona, Colorado, Florida, Hawaii, Idaho, Nebraska, Nevada, North Carolina, Oklahoma, Oregon, Tennessee, Texas, Utah, and Washington. (The District of Columbia—which we neglected of the desk under—can be again above pre-pandemic 2019 energetic stock ranges.)

window.addEventListener(“message”,perform(a){if(void 0!==a.information[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.information[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.information[“datawrapper-height”][t]+”px”;r.type.top=d}}});

The massive image

Over the previous a number of months, the post-boom softening has misplaced momentum, and stock progress has decelerated on a year-over-year foundation. That stated, the nationally aggregated housing market stays gentle. While home prices are declining in some parts of the Sunbelt, a big share of Northeast and Midwest markets are nonetheless eking out modest year-over-year beneficial properties. On the nationwide stage, residence costs are basically flat 12 months over 12 months.

Under is one other model of the desk; this one consists of each month since January 2017.

window.addEventListener(“message”,perform(a){if(void 0!==a.information[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.information[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.information[“datawrapper-height”][t]+”px”;r.type.top=d}}});

Should you’d like to look at the month-to-month state stock figures additional, use the interactive chart under.

Florida—which has been the epicenter of housing market weak point over the previous two years, notably in Southwest Florida—is not seeing the upward burst in stock. Certainly, the intensity of Florida’s housing market correction is easing across many pockets of the state.

Click here to view a sortable model of the chart under.

{kind=link}