Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

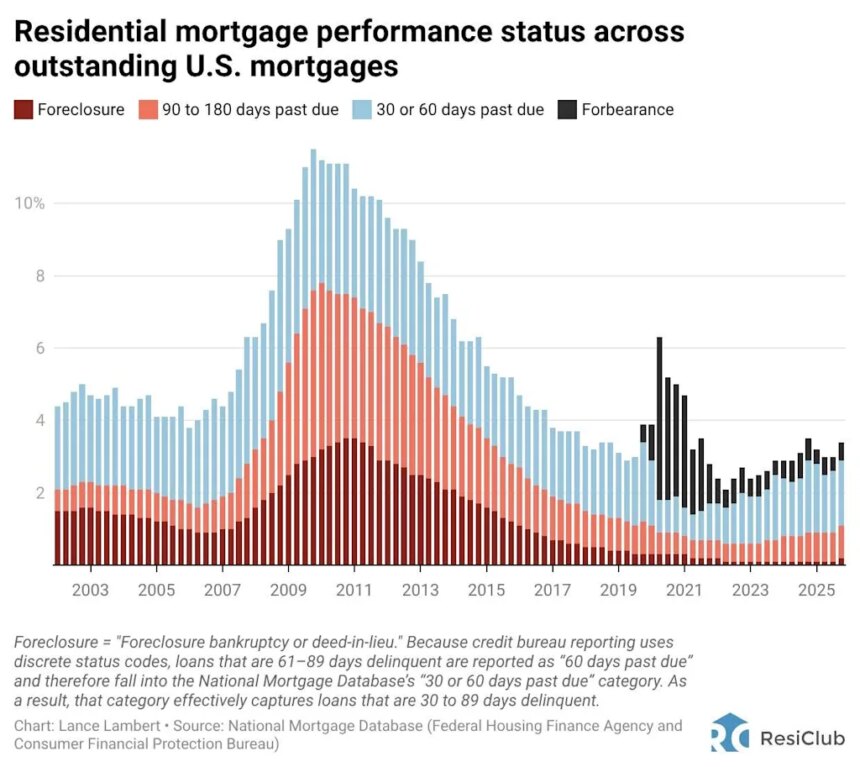

Earlier than a house falls into foreclosures, the warning indicators usually seem months earlier. A borrower first misses a fee or two, touchdown within the 30- or 60-day delinquency bucket. If monetary stress persists, they fall additional behind—90 to 180 days late—and solely round then (lenders typically can’t begin foreclosures till a borrower is no less than 120 days delinquent) does the foreclosures course of usually start.

This development issues as a result of the pipeline of early-stage delinquencies right now tells us an excellent deal about the place foreclosures exercise is headed tomorrow.

Proper now, that pipeline is small by historic requirements—but it surely’s rising. Trying on the Nationwide Mortgage Database, early-stage delinquencies (30 or 60 days late) have been ticking upward since 2022, and extra severe delinquencies (90 to 180 days late) have adopted in variety.

The sample is in keeping with a housing market slowly normalizing after years of extraordinary intervention. When COVID-19 lockdowns started, the federal authorities carried out a nationwide foreclosures moratorium to guard owners from the financial fallout. These protections—together with forbearance applications—had been prolonged a number of instances.

On the similar time, a historic surge in housing demand pushed dwelling costs to new highs throughout the Pandemic Housing Growth, boosting home-owner fairness and holding foreclosures exercise unusually low. The info reveals this clearly: foreclosures and severe delinquency charges cratered to historic lows round 2021.

However in current quarters, foreclosures have steadily returned, inching nearer to pre-pandemic 2019 ranges. That foreclosures rebound picked up tempo in Q1 2025, following the expiration of the moratorium on VA-backed mortgages. As these protections have wound down, the underlying stress that had been deferred—not eradicated—is lastly surfacing within the knowledge.

Nonetheless, perspective is important. Present ranges of mortgage misery stay a fraction of what the nation skilled throughout the 2008 housing bust and the Nice Monetary Disaster, when whole distressed mortgages—the share both going through foreclosures, 90 to 180 days late, 30 or 60 days late, or in forbearance—had been 6.3% in This autumn 2007 and peaked at 11.5% in This autumn 2009, in accordance with ResiClub evaluation. Right this moment’s comparable determine is roughly 2.9%—elevated relative to the pandemic housing growth’s historic low (1.4%), however nowhere close to a systemic disaster.

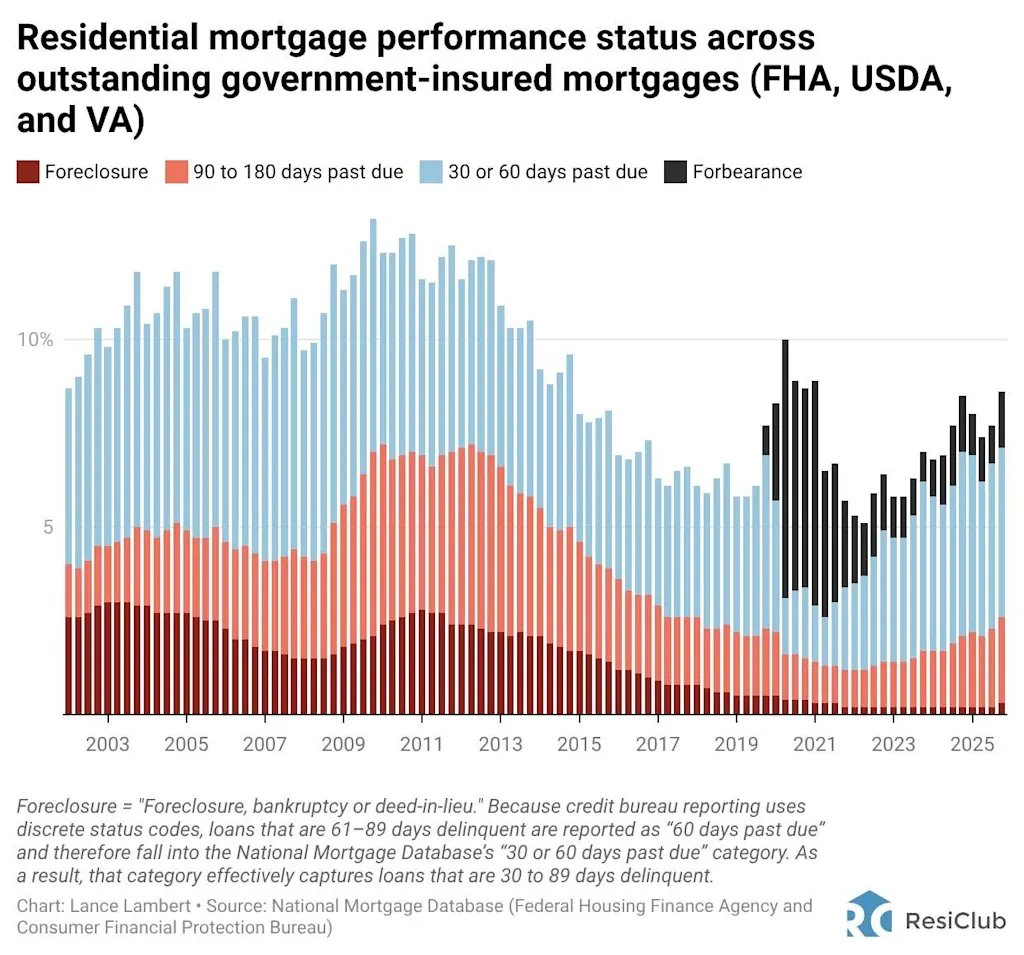

Whereas combination U.S. housing misery nonetheless isn’t that top, there are some pockets of concern with the federal government mortgage applications (FHA, USDA, and VA).

FHA mortgages—that are backed by the Federal Housing Administration and infrequently utilized by first-time or lower-income homebuyers—have seen a notable spike in delinquencies over the previous two years. Remember the fact that FHA mortgages make up a a lot smaller share of total debtors than, say, GSE standard debtors (assured by Fannie Mae/Freddie Mac). In keeping with the Nationwide Mortgage Database, as of This autumn 2025, government-insured mortgages (FHA, USDA, and VA) characterize 23.3% of the nation’s excellent mortgage debt.

How does whole housing misery—the share of all excellent mortgages both going through foreclosures, 90 to 180 days late, 30 or 60 days late, or in forbearance—differ throughout the nation proper now?

Proper now, the best focus isn’t within the largest boomtowns throughout the Pandemic Housing Growth—markets like Cape Coral and Austin, which have been present process post-boom ‘materials’ corrections. As a substitute, the biggest focus of housing misery is in Louisiana and Mississippi, each of which have been hit by important insurance coverage shocks and shopper credit score stress. Many pockets of Louisiana and Mississippi have skilled pricing weak point over the previous few years regardless of not having run up that a lot beforehand, relative to different Solar Belt markets.

See state-level housing misery in This autumn 2025 under.

window.addEventListener(“message”,perform(a){if(void 0!==a.knowledge[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.knowledge[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.knowledge[“datawrapper-height”][t]+”px”;r.type.peak=d}}});

How does housing misery over the previous a number of months evaluate to, say, throughout the early innings of the 2007-2011 housing downturn?

See state-level housing misery in This autumn 2007 under.

window.addEventListener(“message”,perform(a){if(void 0!==a.knowledge[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.knowledge[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.knowledge[“datawrapper-height”][t]+”px”;r.type.peak=d}}});

Complete housing misery throughout most U.S. markets in This autumn 2025 stays a fraction of what it was in This autumn 2007, earlier than the complete weight of the Nice Monetary Disaster had even taken maintain.

The most important exception is Louisiana.

{kind=link}