Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Ever since charges spiked and the Pandemic Housing Increase fizzled out in spring 2022, institutional single-family rental (SFR) operators have pulled method again from shopping for up houses on the resale market—the mathematics simply isn’t as interesting proper now. House costs and rents are not ripping, holding prices (property taxes and insurance coverage) have jumped, capital markets have shifted their consideration elsewhere, and elevated supplies costs make renovations costly.

Within the post-boom setting, many institutional SFR operators turned gentle internet sellers as their regular portfolio acquisitions slowed considerably whereas their routine portfolio culling continued.

Solely, this spring that internet selloff accelerated.

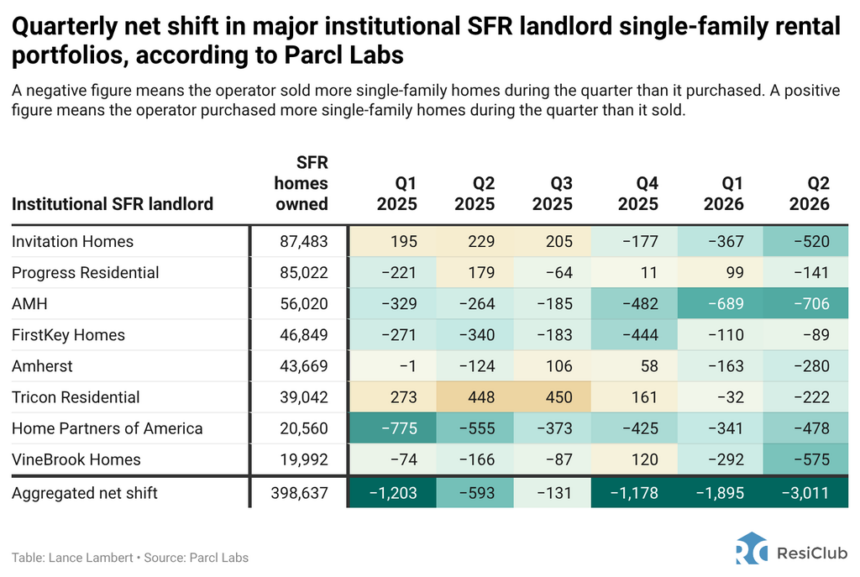

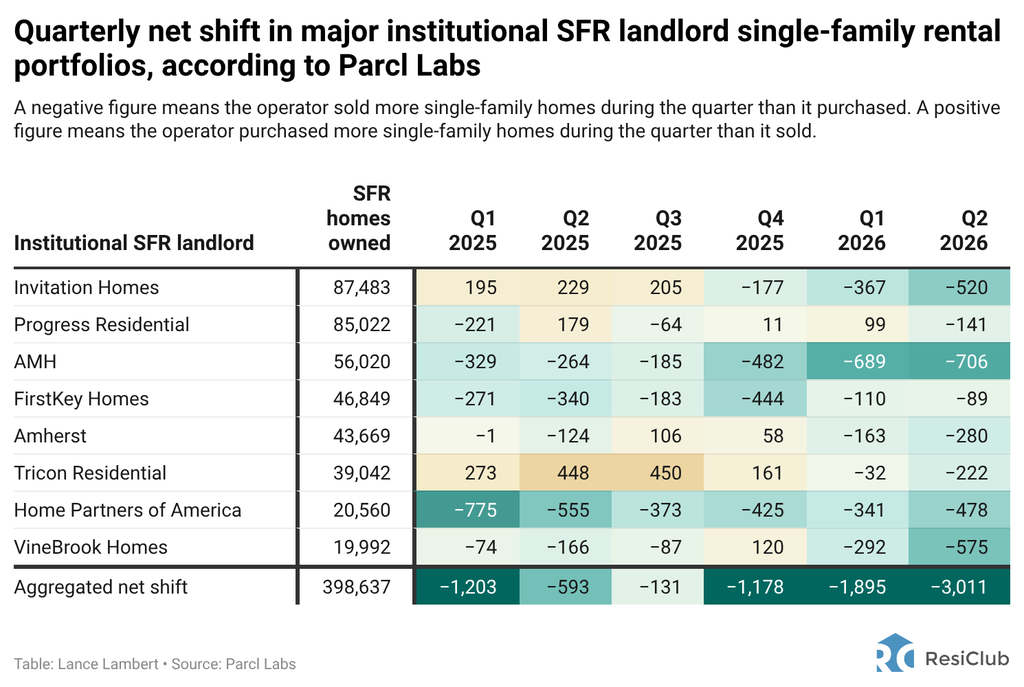

- In Q2 2025, the 8 main institutional landlords tracked by Parcl Labs had been internet sellers of 593 single-family houses.*

- In Q2 2026, the 8 main institutional landlords tracked by Parcl Labs had been internet sellers of three,011 single-family houses.

Why did the institutional internet promoting speed up this spring? Beneath are 4 important elements.

1. The federal push to ban institutional homebuying this 12 months has created a chilling impact

On January 7, President Trump introduced he was taking steps to ban massive institutional buyers from shopping for extra single-family houses and referred to as on Congress to codify it. Then on March 2, Tim Scott (R-SC) and Elizabeth Warren (D-Mass.) launched the revised twenty first Century ROAD to Housing Act, setting the “ban” threshold at 350 houses. The Senate handed it 89–10 in March. However the invoice got here with a catch that alarmed the housing business: whereas build-to-rent was technically exempted (purchases of homes that require major repairs were also exempted), institutional landlords can be required to promote these houses acquired via the exemptions to particular person patrons inside seven years of buy. The National Association of Home Builders withdrew support. A bipartisan group of 76 Home members signed a letter calling the selloff rule a measure that might “effectively halt the production of Build-to-Rent housing nationwide.”

In the end, in May, the Home made a number of modifications, which the Senate later backed, and the invoice is now sitting on President Trump’s desk awaiting his approval. The up to date invoice would nonetheless “ban” massive institutional buyers from buying extra single-family houses, besides via designated exemption pathways—primarily both Construct-to-Hire or Repair-to-Personal. Institutional SFR landlords—outlined by the invoice as entities that management 350 or extra single-family houses—can be allowed to maintain the houses they already personal. The biggest change is that the proposed 7-year selloff requirement has been removed—so Institutional SFR operators can proceed to buy or construct rental houses via the exemption pathways with out a pressured sale after 7 years.

Whereas a number of institutional operators inform ResiClub they’re happy with the place the invoice in the end landed—provided that it creates clear exemption pathways they’ll use to proceed constructing Construct-to-Hire communities, shopping for immediately from homebuilders, and buying resale houses on the open market to renovate and maintain as long-term leases (Repair-to-Hire)—the uncertainty surrounding the invoice’s earlier proposals induced many corporations to progressively put potential offers on maintain this spring, together with canceling some Construct-to-Hire communities. In combination, institutional firms surveyed by ResiClub between April 28 and May 26 advised us they’d delayed or determined to not transfer ahead with greater than 6,000 single-family residence offers—whether or not via Construct-to-Hire or Repair-to-Hire methods—attributable to coverage and regulatory uncertainty.

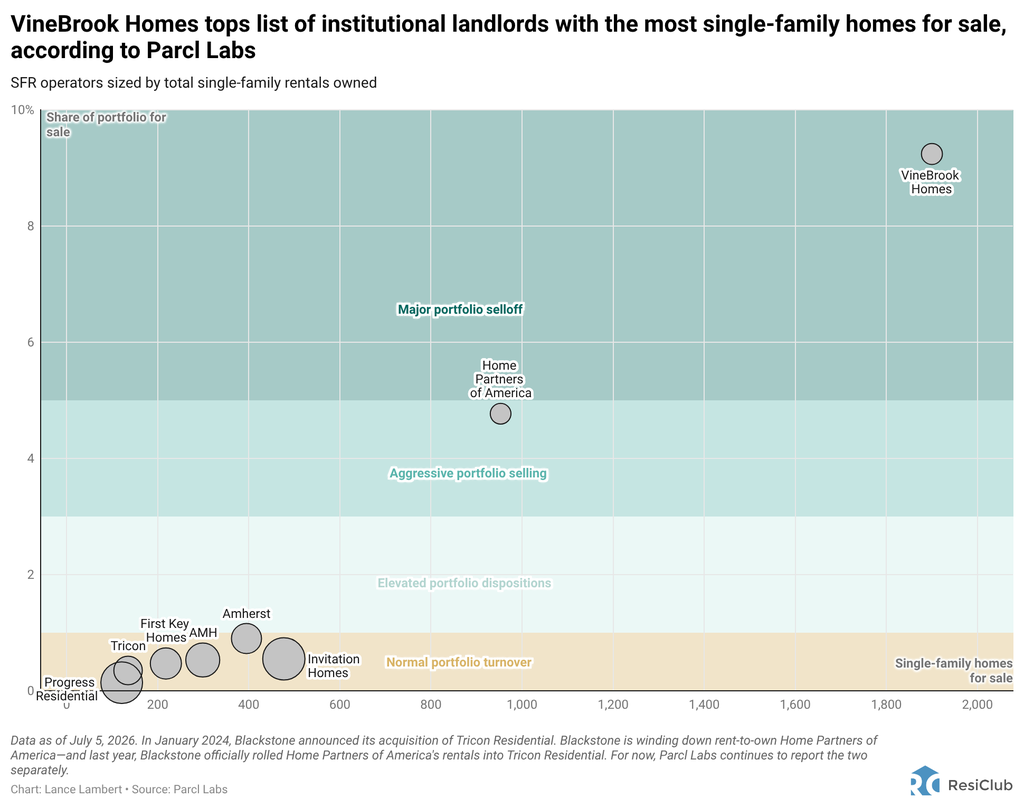

2. Institutional SFR operator VineBrook Properties’ main portfolio selloff is so massive that it’s flattening combination institutional metrics

Click here for an interactive of the scatter plot under

Among the many 8 main institutional SFR operators that Parcl Labs individually breaks out, they’ve 4,498 single-family houses on the market as of July fifth. Of these 4,498 single-family houses on the market, precisely 1,900 are owned by VineBrook Properties (or 42%).

Reviewing VineBrook Properties’ SEC filings from Could 2026, ResiClub discovered that the corporate has accelerated its selloff in current months as a result of it doesn’t have “enough liquidity” to fulfill debt obligations coming due over the following 12 months.

Right here’s what VineBrook Properties wrote in its Could 8, 2026 submitting with the SEC:

“The Firm [VineBrook Homes] has vital debt obligations of roughly $265.9 million coming due inside 12 months of the monetary assertion issuance date, primarily as a result of NexPoint Properties MetLife, which matures on March 3, 2027. As of the date of issuance, the Firm [VineBrook Homes] doesn’t have enough liquidity to fulfill these obligations. To be able to fulfill obligations as they mature, administration intends to guage its choices and should search to: (i) make partial mortgage pay downs, (ii) refinance the NexPoint Properties MetLife Word 1 and (iii) promote houses from its Portfolio and pay down debt balances with the web sale proceed.”

In its May 2026 filings with the SEC, VineBrook additionally advised buyers that it has elevated its selloff with a view to shift capital into “newer houses in BTR communities in larger progress submarkets inside or complementary to our current geographic footprint.”

As of July fifth, VineBrook has 9.2% of its 20,560 single-family portfolio on the market, according to Parcl Labs—which is sufficient to each meet ResiClub‘s label of a “main portfolio selloff” and affect combination institutional statistics.

3. Nonetheless ready for the numbers to work

After accounting for buy value, hire projections, renovations, and capital prices, it’s more durable for institutional buyers to search out the yields they’d wish to justify funding. That’s the driving power behind why institutional homebuying stays subdued since mid-2022. That is neither a window the place institutional buyers can discover resale houses promoting under substitute prices (i.e., the homebuying spree within the 2010s following the foreclosures disaster) nor one the place nationwide residence costs/rents are ripping (i.e., their homebuying spree through the Pandemic Housing Increase).

4. Construct-to-Hire deliveries have rolled over from their growth peak

After seeing an enormous burst through the Pandemic Housing Increase, Construct-to-Hire deliveries have been rolling over since This fall 2023, according to John Burns Research and Consulting.

Invitation Properties—a large institutional single-family landlord—particularly has seen a pointy contraction in its third occasion homebuilder pipeline (i.e. houses it agrees to purchase from homebuilders) since Q2 2024. Invitation Properties stated earlier this 12 months the pullback in BTR offers is tied to its “price of capital” proper now. When an organization’s price of capital is excessive (that means it’s costly to lift fairness or debt to fund new purchases), that’s a market sign that the returns on new investments must clear the next bar. If INVH’s shares are buying and selling at a depressed valuation of their thoughts, issuing fairness to fund acquisitions would dilute shareholders at an unfavorable value. If debt is dear, borrowing to purchase houses eats into returns. In its final earnings name, Invitation Properties executives immediately stated the agency’s competing use of capital proper now’s certainly share repurchases.

Whereas it’s unclear how a lot of a job it’s enjoying, earlier this 12 months, Invitation Homes bought build-to-rent developer ResiBuilt. Whereas ResiBuilt by Invitation Properties will proceed to construct rental communities for out of doors corporations, again in Could, ResiBuilt confirmed to ResiClub that it’s going to additionally construct in-house for Invitation Properties. Studying between the traces, a part of the third-party pipeline drawdown may mirror the corporate’s preparation to shift methods and convey extra of it in-house.

Huge image: As Construct-to-Hire deliveries roll over, amid a interval the place resale acquisitions are already subdued, institutional operators usually tend to change into greater internet sellers—even when a lot of the promoting is simply regular portfolio culling.

{kind=link}